Solution

Together with AI intelligent document processing, IDP, we detect a large number of discrepancies in annual reports such as these examples:- Similarities in annual reports based on historic annual reports for all businesses, e.g has the annual report been copied from another business or part of the data been modified

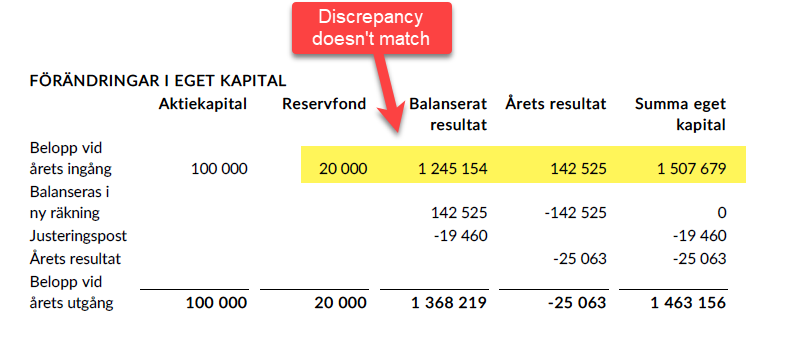

- Summary errors

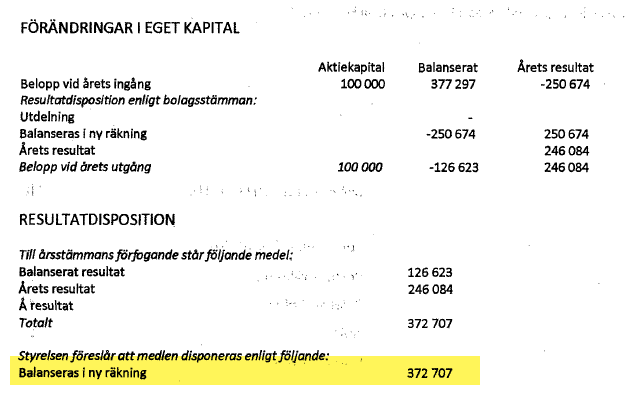

- Unrestricted equity doesn’t balance between the years

- The annual report doesn’t adhere to requirement per local regulations for example in Sweden Annual Accounts Act according to K2 (BFNAR 2016:10) / K3 (BFNAR 2012:1)

- Visually aligning with known accounting systems that typically produce annual reports

Search response for companies

Example

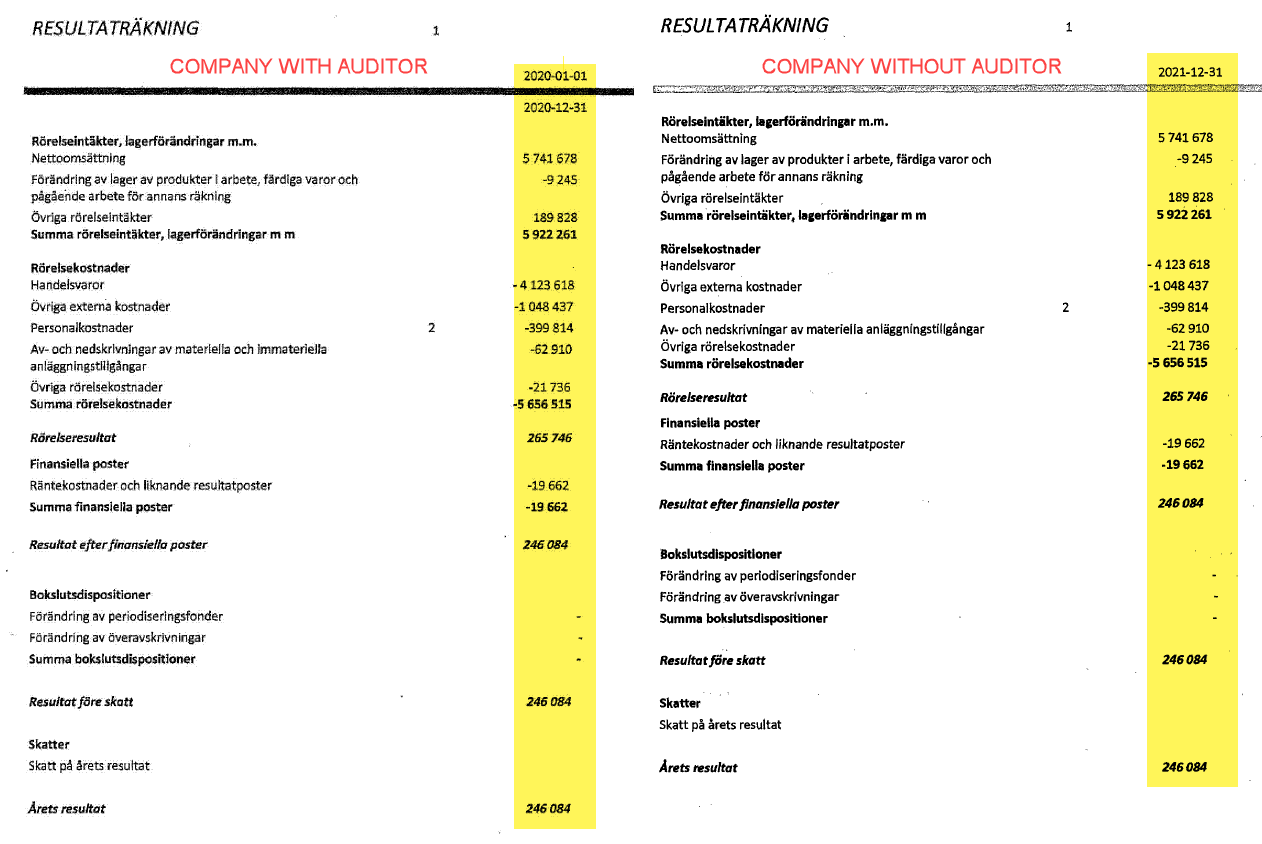

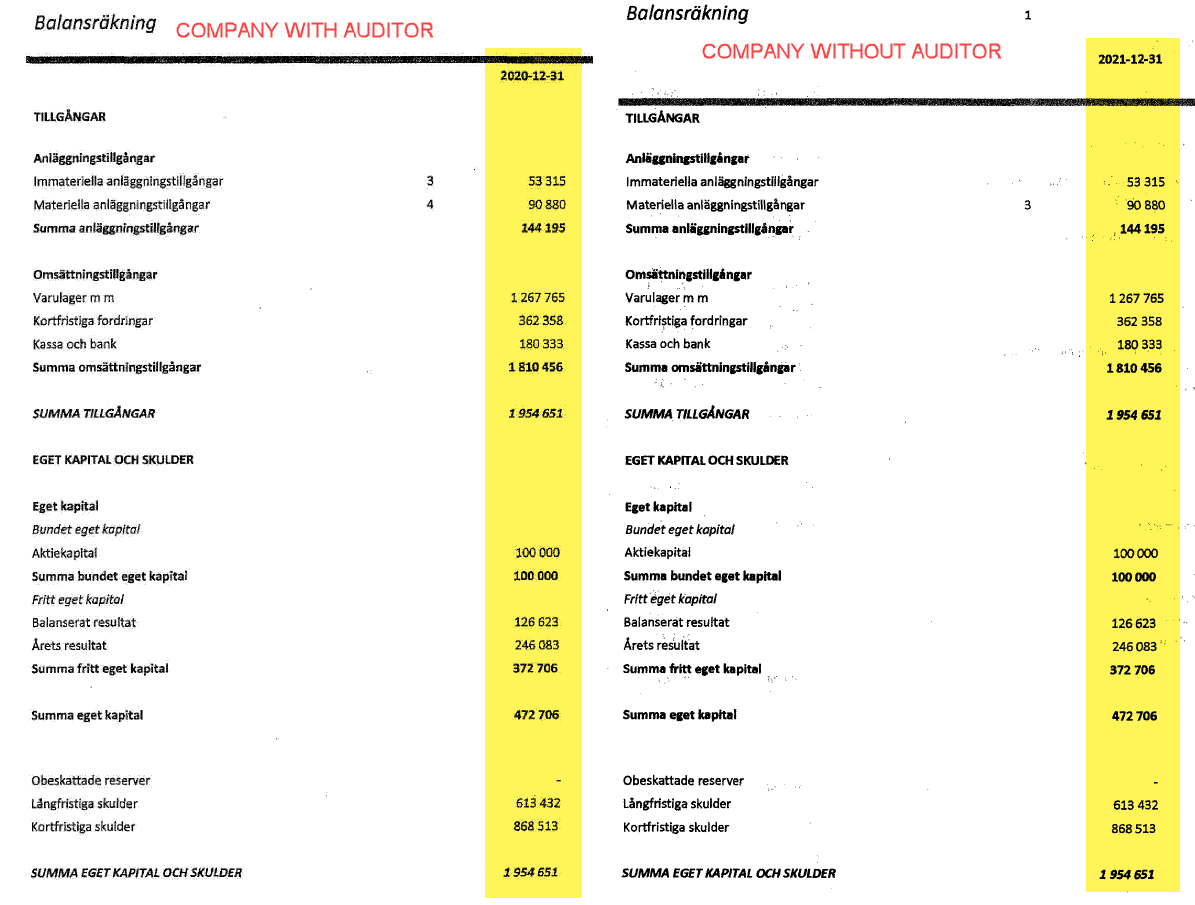

A business with an auditor submits an annual report for the year ending 2020-12-31. The following year another business without an auditor submits a copy of the same annual report but the multi-year overview is wrong and one of the digits in the organizational number has been removed. Visually comparing the result sheet for both businesses you can notice that the rows and amounts are the same with the difference for the year.

How common are financial statement frauds

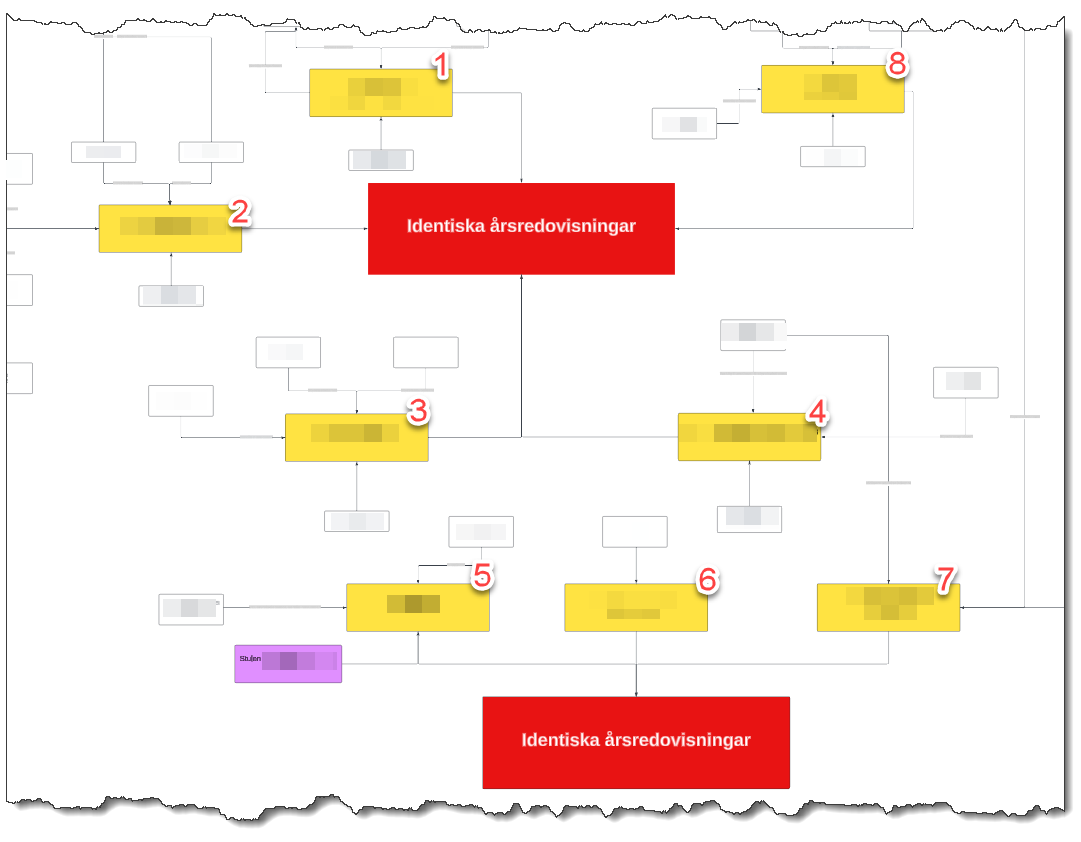

We have learned by looking at discrepancies for the last ten years that financial statement frauds are more common in businesses that has no auditor but they do exist in both. It’s easy to create a new business, submit a fradulent financial report with good looking numbers and get a descent credit score ranking by existing credit reference agencies. The companies may then be used to receive contributions and borrow money and then eventually they go bankrupt. Often we see networks of companies using the same set of financial records but with no links between the company representatives. They exist in various industries and cities. This anonymized example shows a small portion of a network of such companies where eight businesses uses two set of different financial reports but there are no links between the yellow company representatives. These companies could ultimatley be controlled by other individuals.